Nonprofits and the American Rescue Plan Act

President Biden signed the American Rescue Plan Act [March 11, 2021], enacting one of the largest economic relief programs in U.S. history. It is now up to charitable nonprofits to utilize provisions of this new law that are designed to help their organizations and the people they serve survive and recover. … we recap the substance of the legislation, both the overarching portions and then focusing on nonprofit priorities. …

Big picture details

Big ticket itemsThe $1.9 trillion American Rescue Plan Act allocates funds through various programmatic areas, including: | ||

| Stimulus Checks | $400 billion | |

| State/Local Aid | $350 billion | |

| Unemployment | $250 billion | |

| Education | $170 billion | |

| Individual/Corporate Tax Credits | $160 billion | |

| Vaccines & Testing | $125 billion | |

The American Rescue Plan Act, among other things, provides an additional $125 billion in funding for COVID-19 vaccines, treatment, and testing; approves $1,400 stimulus checks per person for most individuals and families; extends additional federal unemployment benefits into September and exempts more than $10,000 in these benefits from federal income taxation; increases the child tax credit and earned income tax credit; and extends the tax credit for nonprofits and other employers that voluntarily provide paid sick leave and paid family and medical leave through September 30, 2021. The law also provides more funding for food assistance, housing and homelessness prevention, the Paycheck Protection Program and the Shuttered Venue Operator Grant program, childcare providers, arts and humanities organizations, the Corporation for National and Community Service, and assistance for nonprofits providing services to survivors of domestic violence and sexual assault.

Treatment of nonprofit priorities

With tens of millions more individuals and families turning to charitable nonprofits for help surviving the pandemic, the nonprofit community came together and advocated forcefully to be included in federal relief legislation. Here are some of the priorities that nonprofit advocacy secured in the American Rescue Plan Act:

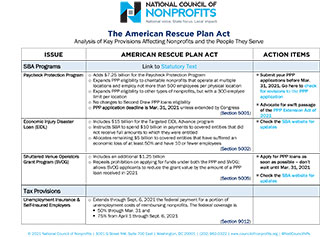

- Paycheck Protection Program (PPP) Loans. The law adds $7.25 billion to the program and expands eligibility to nonprofits with more than 500 employees that operate at multiple locations as long as no more than 500 employees work at any one location. In a win for performing arts nonprofits, the bill allows them to apply for funds under both the PPP and Shuttered Venue Operators Grants (SVOG) program, although a SVOG grant would have to be reduced by the amount of any PPP loan. Although Congress just added billions for more PPP loans, it did not extend the March 31 deadline for submitting loan applications. …

- Federal Unemployment Coverage. This latest COVID relief package extends various federal benefits for unemployed workers through September 6, 2021, including a provision that increases from 50 percent to 75 percent the federal coverage of the unemployment costs of reimbursing nonprofits. The new law also provides continued coverage for self-employed workers and staff of religious and very small nonprofits.

- Aid to State, Local, Tribal, and Territorial Governments. The law provides $350 billion in aid but imposes restrictions on how governments may spend the funds. Permissible uses include providing “assistance to households, small businesses, and nonprofits, or aid to impacted industries,” funding services that governments cut due to declines in revenue brought on by the pandemic, and making “necessary investments” in water, sewer, or broadband infrastructure. The money may not be used to subsidize tax cuts or pay public pension obligations.

- Charitable Giving Incentives. The new law does not expand incentives for charitable giving, but on Tuesday, March 9, Senators and Representatives introduced the Universal Giving Pandemic Response and Recovery Act, 618 and H.R 1704. If enacted, the legislation would allow taxpayers who claim the standard deduction, rather than itemizing deductions, on their tax returns to take a deduction for charitable giving valued at up to one-third of the standard deduction (around $4,000 for an individual filer and $8,000 for married joint filers). This added giving incentive would be available for tax years 2021 and 2022.

Reprinted from the National Council of Nonprofits.

About the author

Related posts

Empowering change: Black-founded nonprofits achieving impact with limited resources

Delve into data on Black-founded nonprofits to discover how they’re resiliently committed to driving impact in the face of funding disparities, limited growth opportunities, and the need for equitable support and investment.

May 6, 2024

Did nonprofit leadership become more racially diverse after 2020?

Is nonprofit leadership more racially diverse than in 2020? Find out by exploring insights derived from demographic data that help explain what recent shifts in nonprofits led by BIPOC CEOs may signal.

May 2, 2024

Are we building the Candid tools you need?

Learn how Candid tools and products are being built to solve for real-world sector needs–and will become unified into our next-generation platform. Get a sneak peek into all that awaits by visiting beta.candid.org.

May 1, 2024

Embracing partnership: A promising paradigm for nonprofit governance

It’s time to revisit traditional nonprofit governance. National Council of Nonprofit’s Donna Murray-Brown explains why a new partnership-driven model between nonprofit board members and staff promises to unlock greater impact.

April 29, 2024

Foundations step up funding to bolster trust in local news

Trust in local news is critical to combating misinformation and keeping the U.S. public informed by a diversity of voices as evidenced by foundations’ funding to sustain today’s local media outlets’ operations.

April 25, 2024

Scaling positive systems change: Addressing underlying conditions and sustainability

Learn why positive systems change for scaling nonprofits’ impact requires holistically addressing underlying issues of power dynamics, public policies, control over resources, and incentive structures.

April 18, 2024

Rose Marie Fisher says:

While this is very good for small businesses, it does not help out our situation. We are an all volunteer organization and our only funds come from sales of our merchandise. We still provide clothing to the needy in our community.