Fragility and resilience: the landscape of nonprofit financial health in the U.S.

The media is full of the economic consequences of the coronavirus. Here in the United States, 40 million people have lost jobs. Prominent businesses—from Hertz to J. Crew—have declared bankruptcy. But thus far there is an eerie silence as to the consequences for nonprofits: will we see mass casualties among the organizations devoted to a better society? It is, of course, too early to say with any certainty what will happen. What we can do is take a rigorous look at the landscape of nonprofit financial health going into this crisis.

In a recent analysis, we looked at the finances of the American nonprofit sector as a whole. When you add up every organization together, the picture is relatively healthy: Over the last twenty years, nonprofits have collectively grown their net assets by more than $1 trillion. In part, this is a consequence of a period of overall economic growth, but it also reflects increasingly sophisticated nonprofit management and governance.

Those aggregate numbers are important; they help us think about our sector as a whole. But this “big picture” obscures a vast diversity of individual experiences. The social sector is large, it contains multitudes: from billion-dollar hospitals to volunteer-run clinics. The wealthiest institutions are likely to survive this crisis. But the same may not be true for many of the smaller organizations that form the sinews of community across the nation.

How might we understand the financial health of nonprofit organizations? My colleagues Carol Brouwer and Anna Koob did an analysis of 315,698 tax-exempt nonprofits which casts some light on the situation. (The set excludes foundations, inactive organizations, and most nonprofits with under $50,000 in annual revenue. In the methodology section you’ll find additional detail.)

This analysis reveals a complex picture. Most American nonprofit organizations are positioned to survive a short financial recession. But even the financial dislocation we’ve already seen is likely to claim thousands of nonprofits. A longer one could be devastating.

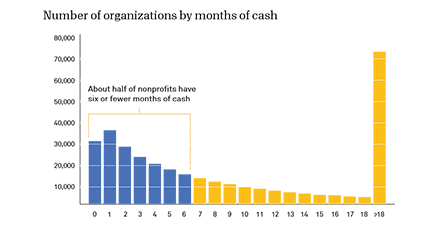

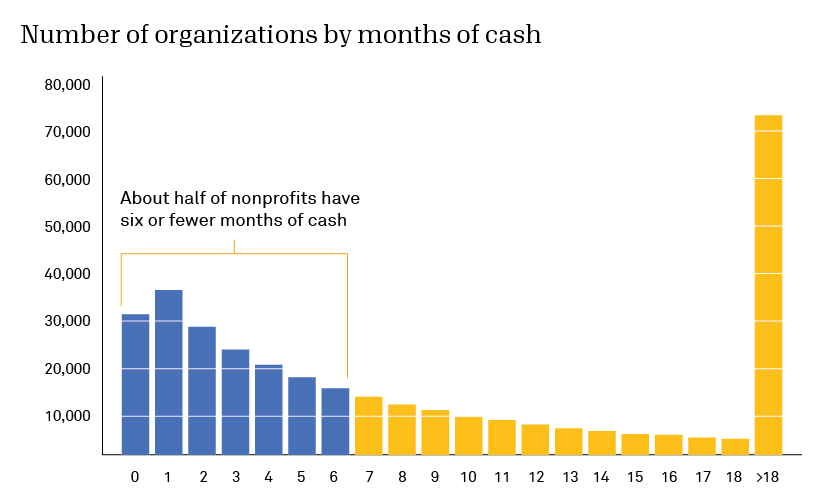

Finding #1: The median nonprofit has about 6 months of cash

We focused our analysis on a common financial metric, “months of cash” (MOC). In simple terms, this metric reflects how long it would take for an organization to run out of money if its revenue went to zero but its expenses stayed the same. In the methodology section, below, we discuss our specific definition of this metric and note some important nuances.

Many experts recommend that organizations aim to have at least six months of cash in reserve. Approximately half of American nonprofits do not meet that threshold. A low number does not necessarily represent inherent fragility or mismanagement. Many of these organizations might have steady revenue even during financial crises and/or the ability to quickly cut costs. Still, this statistic is a reminder that if the coronavirus financial health crisis lasts into 2021, many nonprofits will have passed a point well beyond their financial cushion. On the other end of the spectrum, we see 71,813 nonprofits with more than 18 months of cash.

It is worth noting that this metric is very sensitive to definition. For example, if we include depreciation in our definition of “expenses” we see a much more dire picture. Under that definition, 80% of nonprofits have fewer than three months cash. Depreciation is not a cash expense, so it can be managed in the short-term. But in the long-term, capital bills come due.

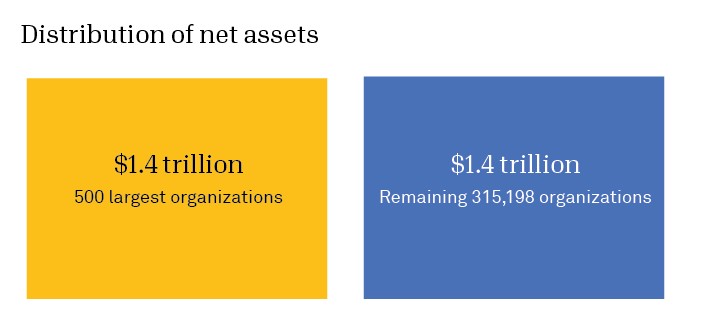

Finding #2: The 500 largest nonprofits have as much “wealth” as the remaining 315,198 organizations

“Net assets” is as close to a proxy as we have for organizational “wealth.” The net assets of this subset of the American nonprofit sector total $2.8 trillion (that’s $2,800,000,000,000). Half of that total is held by the wealthiest 500 organizations, with the remaining 315,198 holding the other half.

This represents a striking distribution of resources. These large institutions include many major universities and hospitals that are critical anchors to communities. For organizations operating at such massive scale, a strong balance sheet is not just desirable, it is necessary. Still, it is no surprise that the relative wealth of these institutions comes under scrutiny at a time like this.

If the financial health crisis extends well into the future, even these wealthier institutions could face questions about whether they need to dip into reserves or even go through the legal process of reassessing how they treat their endowments.

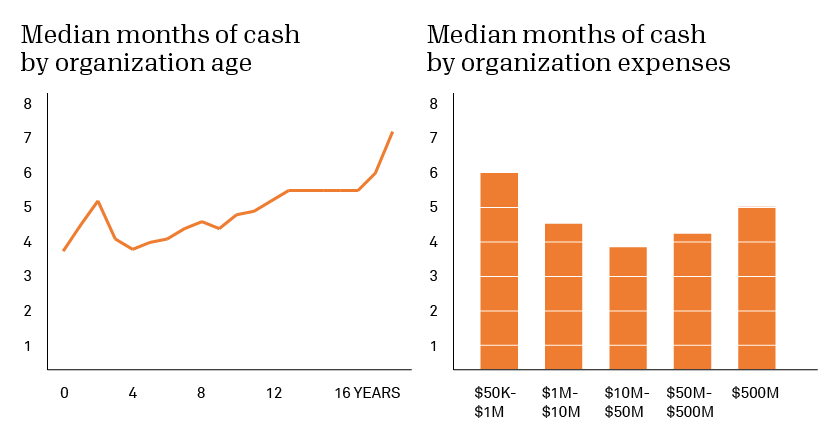

Finding #3: Organizational age and size are modestly correlated with financial health and resilience

As organizations age, we do see a slight increase in median months of cash (MOC). This is to be expected, as organizations have more time to build up reserves—and may become more reluctant to dip into those assets. It is also worth noting the peak in median months of cash among organizations around 2-3 years old—perhaps reflecting those organizations that receive significant start-up funding.

Organizational size has only a modest impact on median months of cash. MOC is a ratio: if the numerator (cash and investments) increases, it is likely that the denominator (expenses minus depreciation) will increase. As a ratio, we would not expect organizational size to be a major driver of MOC. And the variation by size is indeed modest, though we do see that smaller and larger organizations tend to have slightly higher MOC.

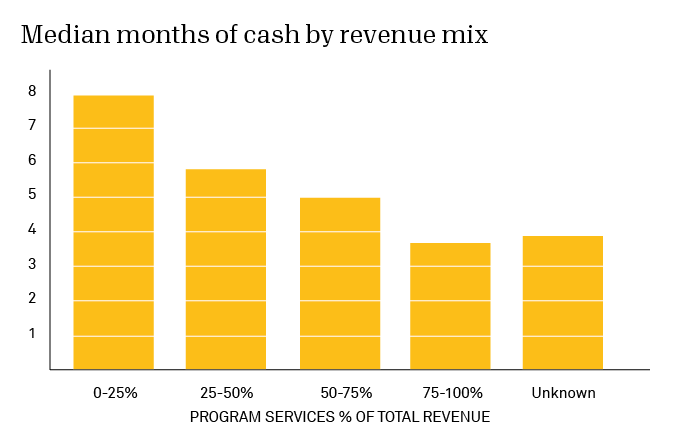

Finding #4: Organizations that rely on program service revenue may face additional financially fragility

Nonprofit organizations rely on a variety of different business models. Some depend primarily on donations—trusting on the generosity of individuals or institutions. But the bulk of the nonprofit sector’s revenue comes from “program services.” This “earned revenue” ranges across a wide range of activities, from an art museum selling tickets to a health clinic providing services that are reimbursed by Medicaid. Such activities are often deeply intertwined with organizational mission and the public good. But they are often quite distinct from the charitable contributions (“contributed revenue”) that make up most of the rest of the nonprofit sector’s revenue.

Both earned and contributed revenue have been compromised by the coronavirus crisis. But anecdotal signs suggest that earned revenue may be hit harder. It’s simply not feasible for a dance company to maintain pre-lockdown ticket revenue if they cannot hold in-person performances. In contrast, many organizations have figured out how to maintain relations with donors virtually.

Our data set shows that organizations that rely primarily on donations tend to have significantly higher MOC. For years nonprofits have been told that earned revenue was more financially sustainable than contributed revenue—and hence required less cushion. Perhaps that will prove to be another myth punctured by the thorned virus in our midst.

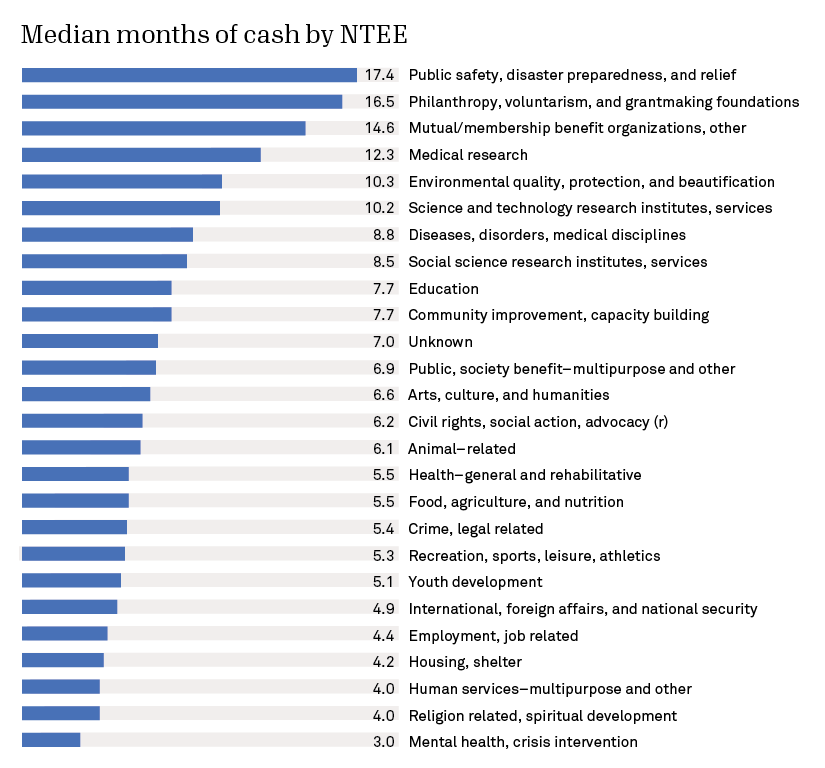

Finding #5: We see significant variation among issue categories

The consequences of business model diversity are clear when you look at nonprofits by issue area. Our dataset shows an extraordinary range: from a median of 3 months of cash for mental health/crisis intervention organizations all the way to 17 months for public safety/disaster preparedness/relief organizations.

This largely reflects the fact that different issue areas lend themselves to different business models. For example, health care organizations often rely on earned income whereas research institutes are more likely to rely on foundation grants. In turn, these different models justify varying levels of savings.

Conclusion

It seems likely that the dislocation of the coronavirus pandemic will lead to the closure of thousands of nonprofit organizations in the United States. But as we watch an even greater number of for-profit businesses collapse around us, we are also reminded of the growing strength of the nonprofit sector. Many nonprofit organizations have spent years being well-managed, well-funded, or just plain lucky. They are ready for a moment such as this.

Others are more fragile. Often organizational vulnerability reflects inequality is society: by definition, organizations rooted in disadvantaged communities have fewer resources to draw from. In this crisis, many communities will lose not just lives, but organizations, too. Just as the nonprofit sector reflects the strength and diversity of our society, it also highlights the work ahead.

Methodology Notes

- The data on which this report is based comes from 315,700 Form 990 and Form 990-EZ IRS filings of public charities (as defined in subsection 501(c)(3) of the IRS code). We have used the most recent filing available to us, going back as far as fiscal year 2015 in some cases when necessary to maximize the record count and diversity of data.

- Small organizations filing a 990-N were omitted as they do not report financial health information. Filings covering substantially more or less than 12 months were removed from the set, as well as those reporting negative values for total expenses or total revenue. Additional filters were applied to exclude organizations believed to be defunct or not in good standing with the IRS.

- The data is presented as reported by the filers, other than occasional errors introduced in assimilation and processing. Numerous records have a total revenue amount that differs from the sum of its parts, although the difference is mostly small. Not all fields map well between form types—the closest available match has been made, sometimes requiring a combination of fields.

- The metric “months of cash” is calculated as follows: (cash + investments) / (revenue-depreciation expenses). It is worth noting that both funds listed as “cash” or “investments” could include legal restrictions. And, as mentioned in Finding #1, including depreciation expenses has a significant impact on the results.

- The issue categorization in Finding #5 was done according to the National Taxonomy of Exempt Entities. Over time we will focusing more of our analysis on the taxonomies in the Philanthropy Classification System.

About the author

Related posts

A collaborative, user-centered approach to website redesigns

If you’re getting started on a website redesign for your nonprofit, consider these five key steps and best practices to help your team prepare for what a new website project will entail and ensure your efforts result in success.

July 24, 2024

Nonprofit fundraising in an election year is especially tough. What can fundraisers do?

Learn how you can overcome challenges in nonprofit fundraising in an election year by adapting your messaging to create impact, especially when engaging donors in swing states.

July 16, 2024

How to run an experiment on your nonprofit’s social media

Learn how to run a social media experiment with expertise guidance to help you better reach, engage, and inspire action among your nonprofit’s donors, supporters, and online community.

July 1, 2024

9 free eBooks to help you brush up on basics and build new skills

Add these nine free eBooks for nonprofits to your summer reading list to brush up on fundraising basics, level up your leadership skills, and learn how to harness innovation for change.

June 26, 2024

Five tips for bringing your nonprofit’s Candid profile to life

Get even more from your nonprofit’s Candid profile with these five tips on how to make your profile stand out to donors and increase the odds of winning over their support.

June 13, 2024

Designing engaging and effective learning experiences

Learn how to create learning experiences, educational materials, and trainings that equip your nonprofit’s staff for success with expert tips from Candid’s instructional designer.

June 5, 2024